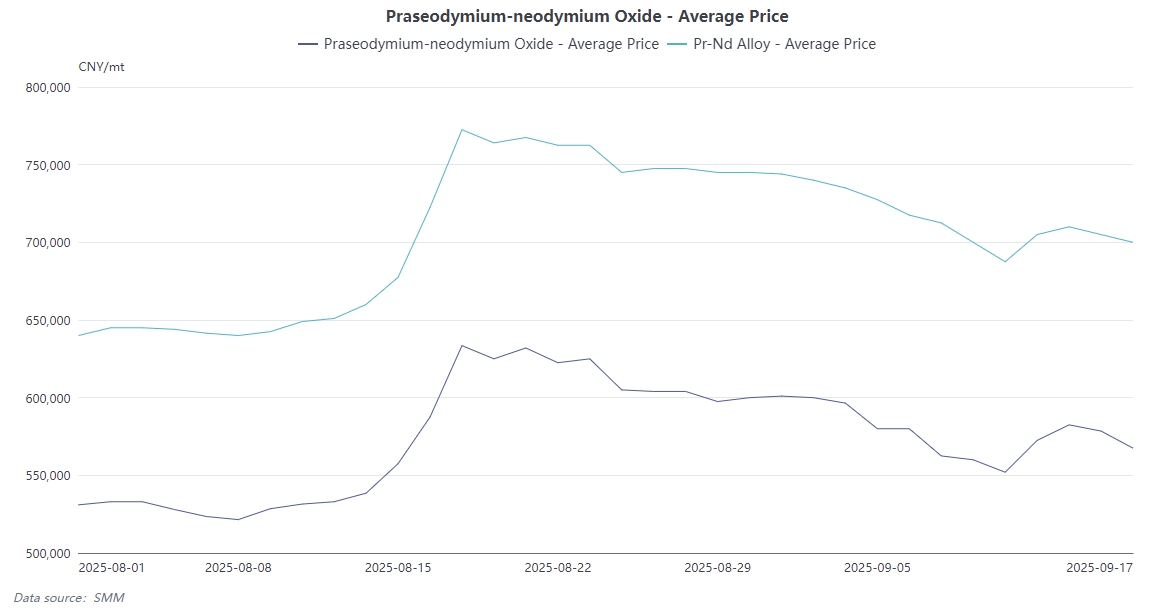

SMM News: On September 16, the Pr-Nd alloy was quoted at 700,000-710,000 yuan/mt, down by 5,000 yuan/mt from the previous day; on September 17, the quote further dropped to 695,000-705,000 yuan/mt, down by another 5,000 yuan/mt. After a rapid rise, the Pr-Nd alloy market experienced two consecutive declines, mainly due to the end of rigid restocking demand and a temporary lack of sustained growth momentum.

I. Behind the Price Pullback: Short-Term Drivers Weaken and Demand Diverges

This price pullback primarily stems from the weakening of the phased restocking drive. In early September, after the price of Pr-Nd alloy pulled back to a relatively low level of 687,500 yuan/mt, large magnetic material enterprises initiated procurement first, driving motor and end-user enterprises to stockpile, which in turn prompted magnetic material enterprises to purchase Pr-Nd alloy, thereby pushing up the overall price. However, this round of restocking is essentially rigid demand, and the actual demand extending from the end-users has not significantly increased. Some enterprises are stockpiling raw material inventory only for overseas orders at year-end, rather than based on continuously robust downstream consumption.

Market wait-and-see sentiment has subsequently intensified, with overall trading volume remaining low. Although the restocking actions by some enterprises once drove an increase in inquiries for mainstream products, the application end has become more cautious in procurement due to the continuous price decline, mostly focusing on consuming existing inventory. Additionally, there is significant divergence within the industry: leading large enterprises continue to see improved operating rates, with overseas orders increasing; while mid-tier and smaller enterprises have orders falling short of expectations, with weaker production.

II. Supply-Demand Pattern: Short-Term Pressure Coexists with Long-Term Potential

From the supply side, policy controls on rare earth mining and separation continue to tighten, with overseas rare earth mining now included in the scope of regulation. Combined with the impact of news regarding some separation plants halting production in Q4 and the evolution of international political situations such as Sino-US rivalry, overall supply remains tight.

On the demand side, the situation is characterized by "short-term pressure, long-term promise." In the short term, end-use demand has failed to follow up consistently, particularly as NdFeB blank production fell 6.8% MoM in August, reducing demand for Pr-Nd alloy by 6.3%. Industry production rose slightly in September to meet the push for annual targets at year-end by end-users and motor enterprises. However, in the medium and long term, demand for high-performance rare earth permanent magnets in sectors such as NEVs, wind power, and heavy industry continues to grow. More imaginatively, emerging fields like humanoid robots and the low-altitude economy, though their growth potential is not yet fully clear, offer additional space that remains to be observed.

III. Industry Divergence: Leadership by Top-Tier Enterprises and Structural Opportunities

The divergence within the rare earth permanent magnet industry is becoming increasingly evident. Top-tier enterprises such as JL MAG Rare-Earth and Zhenghai Magnetic Material each achieved a production volume exceeding 20,000 mt in Q2 2025. Their operating rates continue to improve, boosted by overseas orders, while their technological advantages and large-scale production capabilities have established strong barriers to competition. These enterprises are not only actively expanding production—for instance, JL MAG Rare-Earth is establishing new production lines in Mexico dedicated to the humanoid robot and NEV sectors—but are also reducing costs and enhancing efficiency through technologies such as grain boundary diffusion.

In contrast, small and medium-sized enterprises face greater challenges. Their order volumes fall short of expectations, production remains weak, and they exhibit lower flexibility in raw material procurement and cost control. This divergence also signals a potential further increase in industry concentration, where leading enterprises with high technological barriers and scalable capacity are expected to become more competitive.

Conclusion:Short-term Fluctuations and Medium and Long-term Optimism

In the short term, the market lacks strong positive stimuli, and the demand-boosting effect of the traditional September-October peak season remains to be seen. It is expected that Pr-Nd prices may continue to face some downward pressure from late September to the National Day holiday in early October, but given the tightening fundamentals, the downside room is relatively small. The next concentrated restocking cycle is anticipated to occur from late October to early November.

In the long term, the rare earth industry holds significant development potential. The green energy transition, policies such as the Rare Earths Management Regulations, and new technology applications like humanoid robots and the low-altitude economy will collectively form the foundation of rare earth demand. Additionally, China's strategic positioning and control measures for rare earth resources, including export controls on certain medium-heavy rare earth items, will support a central price increase in the medium and long term. Future prices are expected to rebound steadily within a range acceptable to both upstream and downstream players.